Quick Summary

Corporate Social Responsibility (CSR) spending in India is strictly defined under the Companies Act, 2013, which requires every rupee to be spent in accordance with clear rules on what qualifies and what does not. This guide explains CSR expenditure rules in very simple language so companies can stay compliant and avoid penalties. For both businesses and NGOs, understanding CSR spending can determine whether they can create a positive impact or face significant legal consequences. At NGOExperts, we simplify compliance so you can focus on making a difference. Here is your definitive guide to CSR expenditure rules.

What are the CSR Expenditure

CSR provisions apply to companies that cross any of the prescribed thresholds of net worth, turnover or net profit, as laid down in Section 135. Once any of the criteria are applicable, the company must constitute a CSR Committee, frame a CSR Policy, and ensure that at least 2% of its average net profits (over the last 3 years) are spent on CSR each year.

CSR expenditure rules say that:

- CSR activities must be undertaken in project or programme mode, not as ad hoc or spontaneous/unscheduled donations or events.

- Activities must be related to the list in Schedule VII; though the list is broad, it is not unlimited.

- Spending must be in India, primarily in local areas where the company operates.

Meaning of CSR Expenditure

CSR expenditure means money spent on approved social and environmental activities for the benefit of society, not for direct business gain. Rule 2(1)(d) of the CSR Policy Rules and Schedule VII together define what is treated as CSR and list what is excluded.

In simple terms, CSR expenditure should consist of the following

- Be voluntary social spending over and above statutory obligations.

- Create measurable, long‑term impact through projects in education, health, and rural development.

- Be recorded and reported separately from the normal operating and administrative costs of the company.

What are the Eligible Activities as CSR Spend in India?

As per Schedule VII, the following is an illustrative list of activities that qualify as CSR in India. Common eligible CSR spends include:

- Promoting healthcare, preventive health, nutrition, sanitation, and safe drinking water.

- Supporting education, especially for disadvantaged groups, including special education and employment‑enhancing vocational skills.

- Ensuring environmental sustainability, conserving natural resources, and contributing to funds such as the Clean Ganga Fund.

- Rural development projects and livelihood enhancement for the poor and marginalised.

- Gender equality, women's empowerment and support for shelters, hostels, and old-age homes.

- Contributions to specified funds and other Schedule VII funds for socio‑economic development and relief.

CSR Activities Allowed Under Schedule VII

Here is a simple view of key eligible activities under Schedule VII

| Schedule VII Area | Simple Explanation | Example CSR Spend |

| Health & sanitation | Projects improving health, hygiene, and disease prevention | Free health camps, toilets in schools |

| Education & skills | Schooling, scholarships, skill training | Digital classrooms, vocational centres |

| Environment & sustainability | Protecting nature and the climate | Tree plantation, waste management |

| Rural & slum development | Better basic services in villages and slums | Roads, water, livelihood programmes |

| Support for vulnerable groups | Help people experiencing poverty, SC/ST, women, children, and the elderly | Shelter homes, nutrition for children |

| Disaster relief & funds | Relief during floods, pandemics, etc. | Relief kits, contributions to PM funds |

The Ministry of Corporate Affairs (MCA) has clarified that activities must be explainable under these heads.

What Does NOT Count as CSR Expenditure?

Certain expenses are clearly not treated as CSR, even if they look social at first glance. MCA specifies that the following do not qualify as CSR expenditure

- Activities undertaken in the normal course of business

- One‑off events like marathons, awards, sponsorships of TV shows, and marketing‑type charitable events.

- Expenses to comply with any law, such as labour law compliance, land acquisition or environmental clearance costs.

- Activities that benefit only employees and their families.

- Contributions to political parties or activities benefitting a political party.

- CSR activities outside India, except in limited cases relating to training Indian sportspersons.

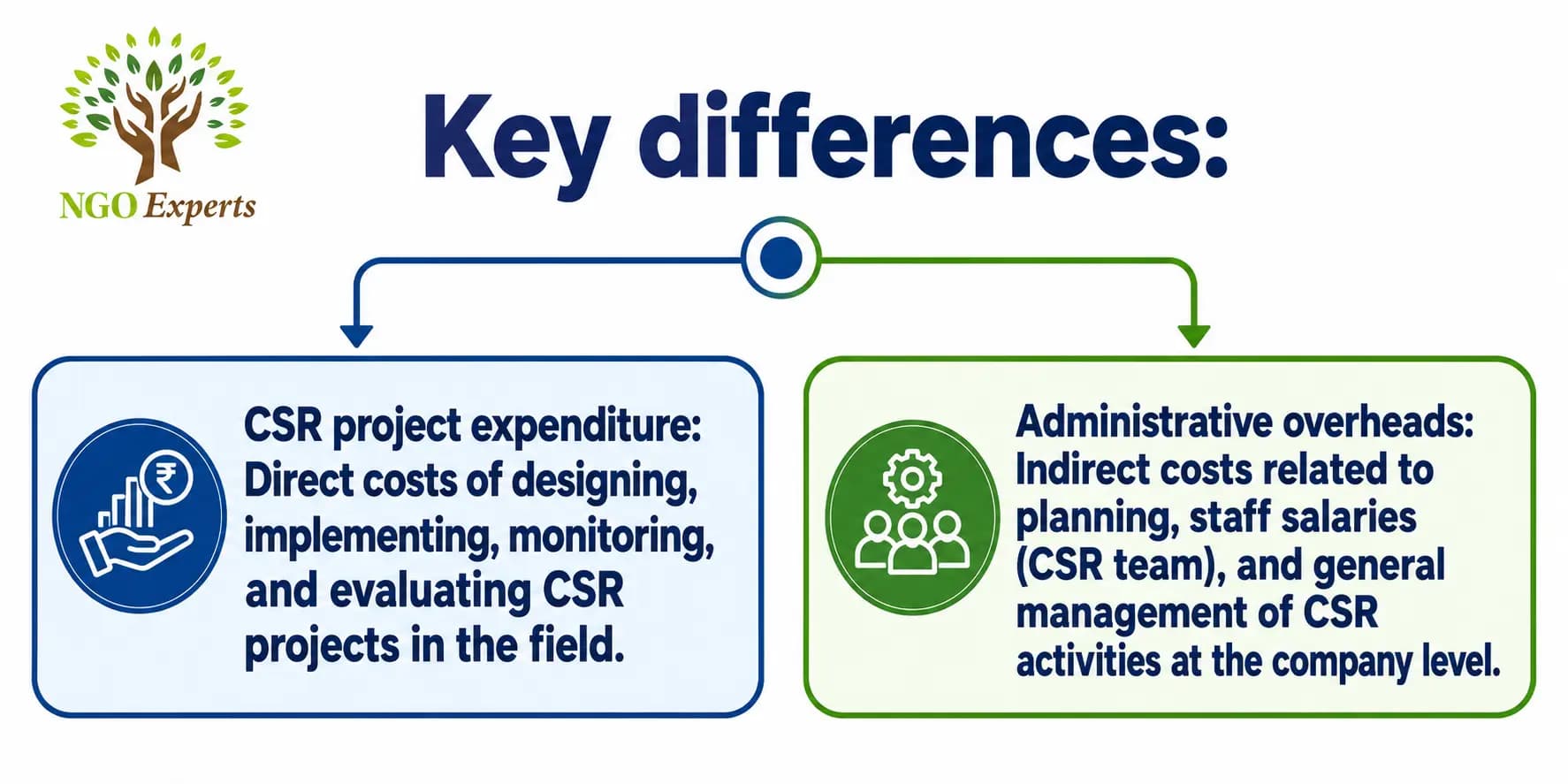

Key Differences between Administrative Overheads and CSR Expenditure

The law draws a clear line between CSR project costs and administrative overheads.

Administrative overheads related to general CSR management cannot exceed 5% of total CSR expenditure for the year.

Administrative overheads related to general CSR management cannot exceed 5% of total CSR expenditure for the year.

Key differences:

- CSR project expenditure: Direct costs of designing, implementing, monitoring, and evaluating CSR projects in the field.

- Administrative overheads: Indirect costs related to planning, staff salaries (CSR team), and general management of CSR activities at the company level.

Monitoring and evaluation of specific CSR projects are treated as part of CSR spend, but total corporate expenses must remain within the limit.

Can Employee Welfare Be Treated as CSR Spend?

As a thumb rule, activities that are exclusively for the benefit of employees and their families do not qualify as CSR, even if they appear to be welfare. MCA clearly excludes employees who only benefit from eligible CSR activities.

However, if a health camp, education project or welfare scheme is designed for the community at large, and employees are only incidental beneficiaries, it can qualify as CSR. Documentation should clearly show that the project targets society, not just the company’s workforce.

Political Contributions & CSR

Any contribution made directly or indirectly to political parties under Section 182 of the Companies Act is not CSR. MCA has clearly stated that political contributions cannot be shown as CSR expenditure under any head of Schedule VII.

Even social initiatives that primarily favour or promote a political party or candidate may be questioned during scrutiny. Companies should keep political donations and CSR budgets completely separate in their books and disclosures.

CSR Capital Assets

CSR funds can be used to create capital assets such as school buildings, community halls, hospital equipment, or other infrastructure. But these assets must be held in the name of specified entities, such as:

- A Section 8 company, registered public trust or registered society with CSR registration.

- Beneficiary communities or public authorities, as allowed under CSR Rules.

CSR assets should not be owned by the company itself or used only for its business benefit. Proper records of capital assets created from CSR funds must be maintained and disclosed as required.

CSR Expenditure on NGOs, Trusts & Section 8 Companies

Companies can implement CSR through:

- Their own Section 8 company was set up as a non‑profit.

- Registered public trusts or societies with the required CSR registration and track record.

MCA clarifications require implementing agencies to be registered on the MCA CSR portal and to meet conditions such as a minimum three‑year track record for certain entities.

Unspent CSR Amount: Transfer Rules & Timelines

If a company cannot spend the full CSR obligation in a year, strict transfer rules apply.

- For non‑ongoing projects, the unspent amount must be transferred to a Schedule VII fund within 6 months from the end of the financial year.

- For ongoing projects, the unspent amount must first be transferred to a special Unspent CSR Account within 30 days of the end of the financial year.

- The amount in the Unspent CSR Account must be used within 3 financial years; failing which, it must be transferred to a Schedule VII fund within 30 days after the end of that period.

These timelines can not be overlooked and must be closely monitored by regulators.

Latest MCA Clarifications on CSR Expenditure Rules

The Ministry of Corporate Affairs (MCA) has issued general circulars and detailed FAQs to address confusion around CSR. Key clarifications include:

- CSR spending cannot be on activities beyond Schedule VII, though the Schedule must be interpreted liberally within its scope.

- One‑off events, normal business activities, employee‑only welfare, and political contributions are not CSR.

- Salaries of dedicated CSR staff and the proportionate volunteer time can be counted as CSR project costs, subject to the rules.

- Unspent CSR rules, implementing agency registration, and the treatment of capital assets created with CSR funds are clearly addressed in the 2021

Conclusion

CSR expenditure rules in India are now very structured, and regulators expect companies to plan CSR like any other core function, with clear projects, proper documentation and timely compliance. By aligning every rupee of CSR spend with Schedule VII, avoiding ineligible expenses, and adhering to unspent fund and reporting rules, companies can create genuine social impact while remaining fully compliant. Don't risk fines or compliance headaches, let NGOExperts handle your CSR strategy from planning to reporting.

Frequently Asked Questions

Can we carry forward excess CSR spend?

Yes, if you spend more than 2%, the excess can be set off against the requirements of the next 3 financial years.

Is GST included in CSR spend?

Yes, the GST paid on goods and services for CSR projects is considered part of the CSR expenditure.

Can we spend CSR funds on our own employees?

No, activities benefiting only employees do not qualify.

Do we need a CSR Committee if our spending is small?

If your CSR obligation is less than ₹50 Lakh, you don't need a committee; the Board can handle the duties.

Can an NGO without CSR-1 accept CSR funds?

No, it is legally mandatory for an NGO to have an active CSR-1 registration to receive and execute.

Author

Aabha Garg

A Content Strategist at NGOExperts, who focuses on NGO registration, 12A and 80G registration, FCRA compliance, income tax filing for non-profits, and CSR funding guidelines in India. I research and write our compliance guides in collaboration with our in-house Chartered Accountants and Company Secretaries, so every article reflects current tax and regulatory requirements for the NGO and non-profit sector.

Written by Aabha Garg. Last updated on July 2, 2026