Quick Summary

Whether you're passionate about women's empowerment, rural development, or financial inclusion, starting a microfinance company under Section 8 is the most effective way to turn your vision into reality.

If you're looking to establish a non-profit organisation focused on providing financial services to underserved communities, understanding the Section 8 microfinance company registration process is essential.

In this guide, we'll walk you through everything you need to know about registering a Section 8 microfinance company, from the basic requirements to the latest regulations.

What is a Section 8 Microfinance Company?

Starting a microfinance company under Section 8 is one of the most rewarding ways to contribute to financial inclusion in India. A Section 8 company is a special type of non-profit organisation registered under the Companies Act, 2013. When combined with microfinance operations, it can provide small loans and financial services to economically disadvantaged groups without any motive of earning profits.

In simple terms, a Section 8 microfinance company structure offers the credibility of a registered company while maintaining a charitable purpose. Many successful organisations have chosen this route to make a genuine difference in rural and semi-urban areas. However, it is noteworthy to say that Section 8 companies enjoy certain exemptions, including lower stamp duty in many states and exemption from minimum capital requirements, making them financially accessible for social entrepreneurs.

Section 8 Microfinance Company Registration Online

With the rise of digital transformation, the Section 8 company registration process is no longer complex or time-consuming.

In fact, with the benefit of digitalisation, the company registration can be done online now in a much simpler and quicker way. You can now complete most steps through the Ministry of Corporate Affairs (MCA) portal without visiting government offices repeatedly.

The online section 8 microfinance company registration process involves submitting digital forms, uploading required documents, and tracking your application status in real time. This has significantly reduced the registration timeline from several months to just 15-30 days in most cases.

Documents Required for Section 8 Microfinance Company

Setting up a Section 8 Microfinance Company in India requires specific documentation. Here's what you'll need:

For the directors:

- PAN Card and Aadhar Card copies for each director

- Recent passport-sized photographs

- Bank statement showing address (must be recent, within last 2 months)

- Passport copy (for Indian nationals) or notarized/apostilled passport (for foreign directors)

- Digital Signature Certificate (DSC) for online filing with the Ministry of Corporate Affairs

- Director Identification Number (DIN) for each director

Constitutional Documents:

- Memorandum of Association (MOA) that clearly outlines your microfinance objectives and charitable purposes

- Articles of Association (AOA) defining how the company will be managed and governed

- Approved company name from the MCA

Have Questions?

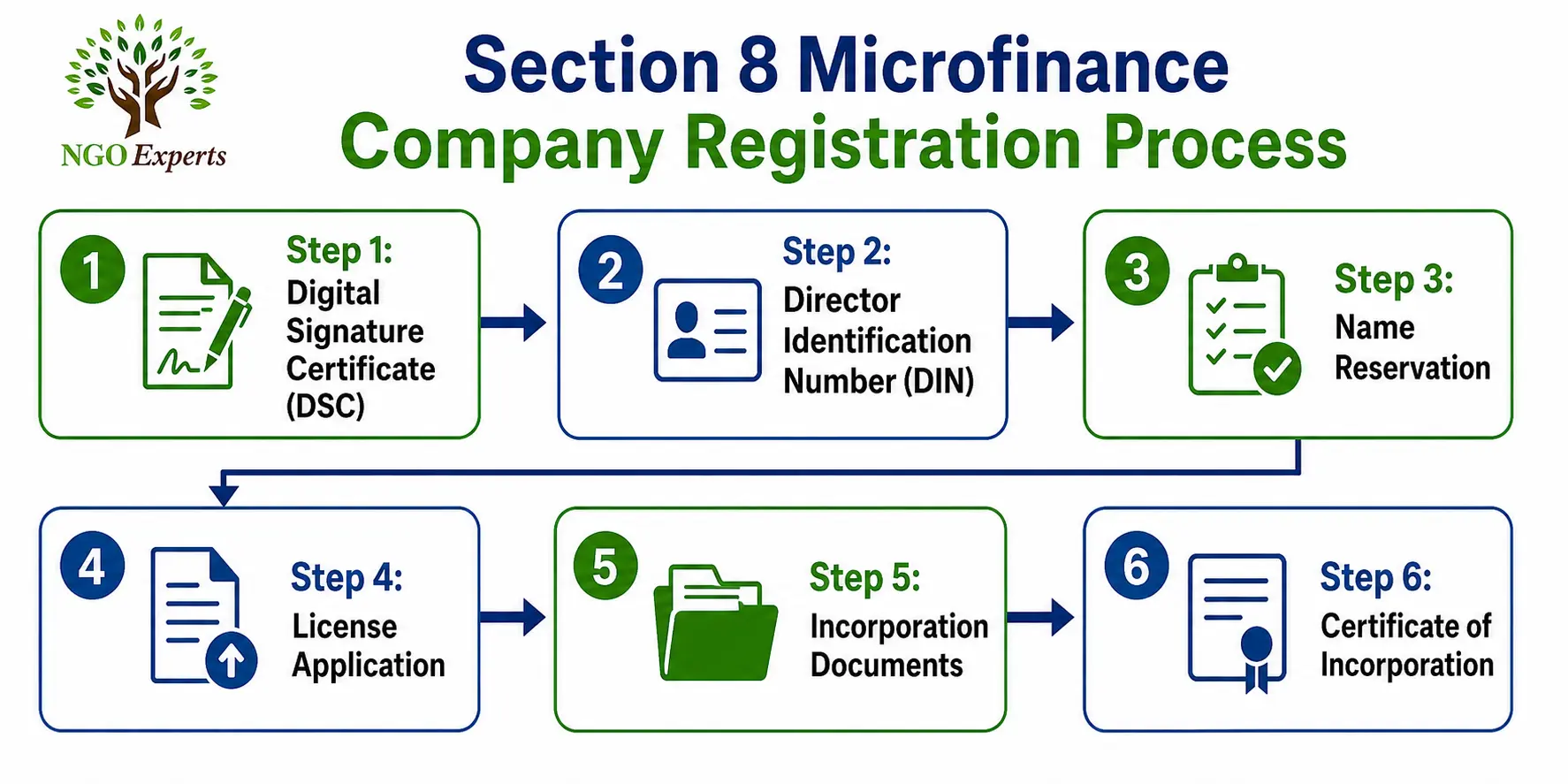

Section 8 Microfinance Company Registration Process

To begin with the registration, here is the complete breakdown of the Section 8 microfinance registration process into manageable steps:

Step 1: Digital Signature Certificate (DSC) First, you'll need to obtain a Digital Signature Certificate for the proposed directors. This is mandatory for filing online applications and typically takes 2-3 days to acquire.

Step 2: Director Identification Number (DIN) All directors must have a DIN. If they don't already have one, you can apply through the MCA portal.

Step 3: Name Reservation Choosing the right name is crucial. You'll need to file Form RUN (Reserve Unique Name) with at least two name options. Remember, your name must include "Foundation," "Association," or similar words, and should clearly reflect your microfinance objectives.

Step 4: License Application. You need to apply for a license from the Central Government through Form INC-12. You'll need to submit your proposed Memorandum of Association (MOA) and Articles of Association (AOA) showing your non-profit charitable objectives.

Step 5: Incorporation Documents Once you receive the license approval, you'll file Form INC-13 (Section 8 Company Incorporation) along with required documents, including MOA, AOA, registered office proof, and consent letters from directors.

Step 6: Certificate of Incorporation After verification, the Registrar of Companies will issue your Certificate of Incorporation, officially establishing your Section 8 microfinance company.

Rules for Section 8 Microfinance Companies

Operating a Section 8 microfinance company comes with specific rules that ensure the organization stays true to its social mission. Understanding these rules is essential for long-term compliance.

- It cannot pay dividends or share profits with members, as everything gets reinvested into the company's social goals, like microfinance for the poor.

- To form a Section 8 microfinance company, at least 2 directors and 2 members are required to incorporate, where 1 director must be an Indian resident.

- All income must promote the company's objectives (e.g., financial inclusion, poverty alleviation); no personal gains allowed.

- Cannot change the Memorandum of Association (MOA) or Articles of Association (AOA) without prior approval from the Central Government (via the Regional Director).

Latest RBI Guidelines for Section 8 Company

If you're planning to operate as a microfinance entity, staying updated with the latest RBI guidelines for a Section 8 company is crucial. The Reserve Bank of India has specific regulations for entities involved in lending activities.

Key RBI Guidelines

- NBFC-MFI Registration: Section 8 companies must register as NBFC-MFI if lending activities cross specified thresholds

- Minimum Capital: Maintain minimum net owned funds of Rs. 5 crore

- Qualifying Assets: At least 75% of loans must be to low-income borrowers (qualifying assets)

- Interest Rate Caps: Adhere to prescribed interest rate ceilings on loans

- Transparent Pricing: Clearly disclose all charges, processing fees, and interest rates to borrowers

- Customer Protection: Implement grievance redressal mechanisms and borrower rights protection

Have Questions?

Benefits of Section 8 Microfinance Company Registration

1. Easier Setup & Lower Costs

Zero Minimum Capital: Section 8 Microfinance structure doesn't require a huge capital Unlike a regular NBFC-MFI, which demands at least ₹5 crore to start, a Section 8 MFI has zero minimum capital requirement. This makes it accessible for social missions.

Lower Registration Costs: Setting up costs just ₹40,000–₹80,000, way less than the lakhs you'll spend on a standard NBFC license.

2. Operational Flexibility

Collateral-Free Loans: These companies offer loans without needing collateral, making them perfect for small businesses or individuals who don't have assets to pledge.

Flexible Lending Limits: You can lend up to ₹50,000 for small business needs and up to ₹1.25 lakh for housing, based on current guidelines.

3. Tax & Financial Benefits

Tax Exemptions: Get exemptions on your "surplus" (that's profit) under Sections 12A and 80G. Plus, your donors can claim tax deductions for their contributions.

Access to CSR Funding: As a section 8 microfinance, you're eligible for CSR funds, corporate grants, and donations, thereby opening doors to steady support.

Foreign Investment (FCRA): With FCRA registration, accept foreign grants and donations to fuel your microfinance work.

4. Legal & Structural Advantages

Limited Liability: Directors' and members' personal assets can be safeguarded; their only risk is what they invest in the company.

Credibility: The "Section 8" license is like a government stamp of trust, boosting confidence from donors, banks (for loans), and rural communities.

Section 8 Microfinance Company Interest Rate

The Section 8 microfinance company's interest rate should remain reasonable and transparent. RBI expects microfinance institutions to avoid excessive exploitation of borrowers.

Important Points About Interest Rates

- Interest rates must be disclosed clearly

- Processing charges should be transparent

- Hidden penalties are not allowed

- Borrowers should receive proper loan cards

The applicable section 8 microfinance company interest rate depends on operational costs, borrower profile, and RBI norms.

Conclusion

Section 8 microfinance company registration opens doors to making a real difference in financially underserved communities. While the process involves multiple steps and regulatory compliance, it's entirely manageable by partnering with a professional CA or legal consultants like NGOExperts.

Remember, the key to success lies not just in registration but in understanding and following the rules, staying updated with RBI guidelines, and maintaining unwavering focus on your social mission.

Frequently Asked Questions

Section 8 companies under the Companies Act, 2013, operate as nonprofits providing microloans to low-income groups for poverty alleviation. They reinvest all profits into social goals without paying dividends.

The approximate section 8 microfinance company registration fees range between ₹40,000 and ₹80,00,0 depending on professional and government charges.

Yes, Section 8 companies can engage in microfinance activities in India as nonprofit entities focused on financial inclusion and poverty alleviation.

The latest RBI guidelines on the operations of section 8 microfinance companies include borrower protection norms, transparent pricing, qualifying asset criteria, and registration requirements for larger lending operations.

The Section 8 microfinance company's interest rate should be reasonable, transparent, and compliant with RBI norms to protect borrowers from excessive charges.