Quick Summary

The Income Tax Department introduced a new registration regime for NGOs, Section 10AB vs. 10AC. NGOs, trusts, societies, and Section 8 companies rely on Forms 10AB and 10AC to secure and maintain tax exemptions under Sections 12AB, 80G, and 10(23C) of the Income Tax Act and a small mistake may cause loss of tax exemption, donor distrust, and compliance notices.

Form 10AC is the official approval order issued by the Principal Commissioner or Commissioner after your initial application, confirming your registration and specifying its validity period. Form 10AB, on the other hand, is the online application you use to renew, convert provisional status to regular, re-register, and activate inoperative approvals. The key difference between the two is that 10AC grants tax-exempt status, while 10AB ensures continuity. Common risks for both include missed deadlines and mismatches, which can result in penalties, including registration cancellation and taxable income.

Overview

NGOs, trusts, societies, and Section 8 companies rely on Forms 10AB and 10AC to secure and maintain tax exemptions under Sections 12AB, 80G, and 10(23C) of the Income Tax Act. Form 10AC is the official approval order issued by the Principal Commissioner or Commissioner after your initial application, confirming your registration with a validity period. Form 10AB, on the other hand, is the online application you use to renew, convert provisional status to regular, re-register, and activate inoperative approvals. The key difference between the two is that 10AC grants tax-exempt status, while 10AB ensures continuity. Common risks for both include missed deadlines and mismatches, which can result in penalties, including registration cancellation and taxable income.

What is Section 10AB under the Income Tax Act?

Form 10AB is an online application filed by NGOs, trusts, and institutions to convert provisional registration into regular registration, renew expiring registrations, reactivate inoperative approvals, or re-register after changing objects. It is common to say "10AB registration," meaning your organization has applied or is applying through Form 10AB for continued tax‑exempt status under the relevant sections.Without a timely 10AB filing, earlier exemptions under 10(23C) / 12A / 80G can lapse, and your income may become taxable.

What is Section 10AC under the Income Tax Act?

When your trust or NGO first applies for registration, the Commissioner checks your documents and, if satisfied, issues an order in Form 10AC with conditions and a validity period. This Form 10AC order is proof that you are registered and can claim income‑tax exemption and donor benefits under the relevant sections.The registration granted under 10AC is time‑bound and must be renewed later through Form 10AB.

Difference between 10 AB and 10 A

| Point | Form 10AC or 10AC Registration | Form 10AB or 10AB Registration |

| Basic nature | Order issued by the department | Application filed by NGO/trust |

| Stage of lifecycle | First approval or registration | Conversion, renewal, activation, re-registration |

| Who issues / files | Issued by PCIT/CIT | Filed online by the NGO/trust |

| Linked sections | 10(23C), 12AB, 80G | 10(23C), 12AB, 80G |

| Role | Grants provisional/regular registration | Keeps that registration alive and updated |

| Used when | You apply for the first time through Form 10A | After the initial grant or provisional approval ends |

| Evidence you show to donors | Copy of 10AC order | Copy of renewed approval based on 10AB |

In simple terms: 10AC provides the registration; 10AB helps you keep it valid and compliant over time.

Applicability of Form 10AB vs Form 10AC for NGOs & trusts

There are certain scenarios where both forms are relevant without any distinction.

- Charitable and religious trusts.

- Registered societies and Section 8 companies carrying out charitable purposes.

- Educational institutions, universities, and hospitals seeking exemption under Section 10(23C).

But you typically encounter scenarios where only Form 10AC is applicable, while in some cases, only Form 10AB is required.

Form 10AC when:

- You file your first‑time registration under Section 12AB / 10(23C) / 80G (usually through Form 10A).

- The Commissioner approves and issues 10AC as the registration order.

Form 10AB when:

- You have provisional registration and must convert it to regular registration.

- Existing regular registration is expiring and needs renewal.

- Registration became inoperative due to dual approval ( 10(23C) and 10(46)), and you want it activated.

- You changed your objects and must get re‑registration under new conditions.

Who is required to file Form 10AB?

You must file Form 10AB online if your NGO or trust falls into any of these categories:

- Already has provisional registration and wants to convert to regular registration, usually within 6 months of the commencement of activities or before provisional registration expires, whichever is earlier.

- Holds existing registration/approval under 10(23C), 12A/12AB or 80G that is due to expire and must be renewed for another term.

- Has an inoperative registration (for example, due to overlap with Section 10(46)) and now seeks activation.

- Has modified its objects, and the new objects do not fully match the conditions on which registration was originally granted, requiring re‑registration.

These situations primarily involve NGOs, charitable trusts, religious institutions, educational institutions, and hospitals claiming exemptions, not regular for-profit companies.

Who is required to obtain Form 10AC?

You do not file Form 10AC; the approval order is issued to you upon successful registration.

You will receive a 10AC order if:

- You apply for first‑time registration/approval under Section 12AB, 10(23C), or 80G through the prescribed forms.

- The Commissioner is satisfied with your trust deed, activities, and documents and grants approval.

This order mentions your:

- PAN and name of trust/NGO.

- Section under which you are registered.

- Type of registration (provisional or regular).

- Validity period and conditions for compliance.

Validity period of 10AB and 10AC registrations

10AC‑based registration validity

Provisional registration is generally valid for up to 3 years. Regular registration granted via 10AC usually has a validity of 5 years, after which 10AB must be used for renewal.

10AB‑based approvals: When you apply through Form 10AB and the department grants renewal or regular registration, that approval is again generally valid for 5 years. If 10AB is not filed within the prescribed timelines, the registration may lapse, and you may have to apply afresh as a new applicant.

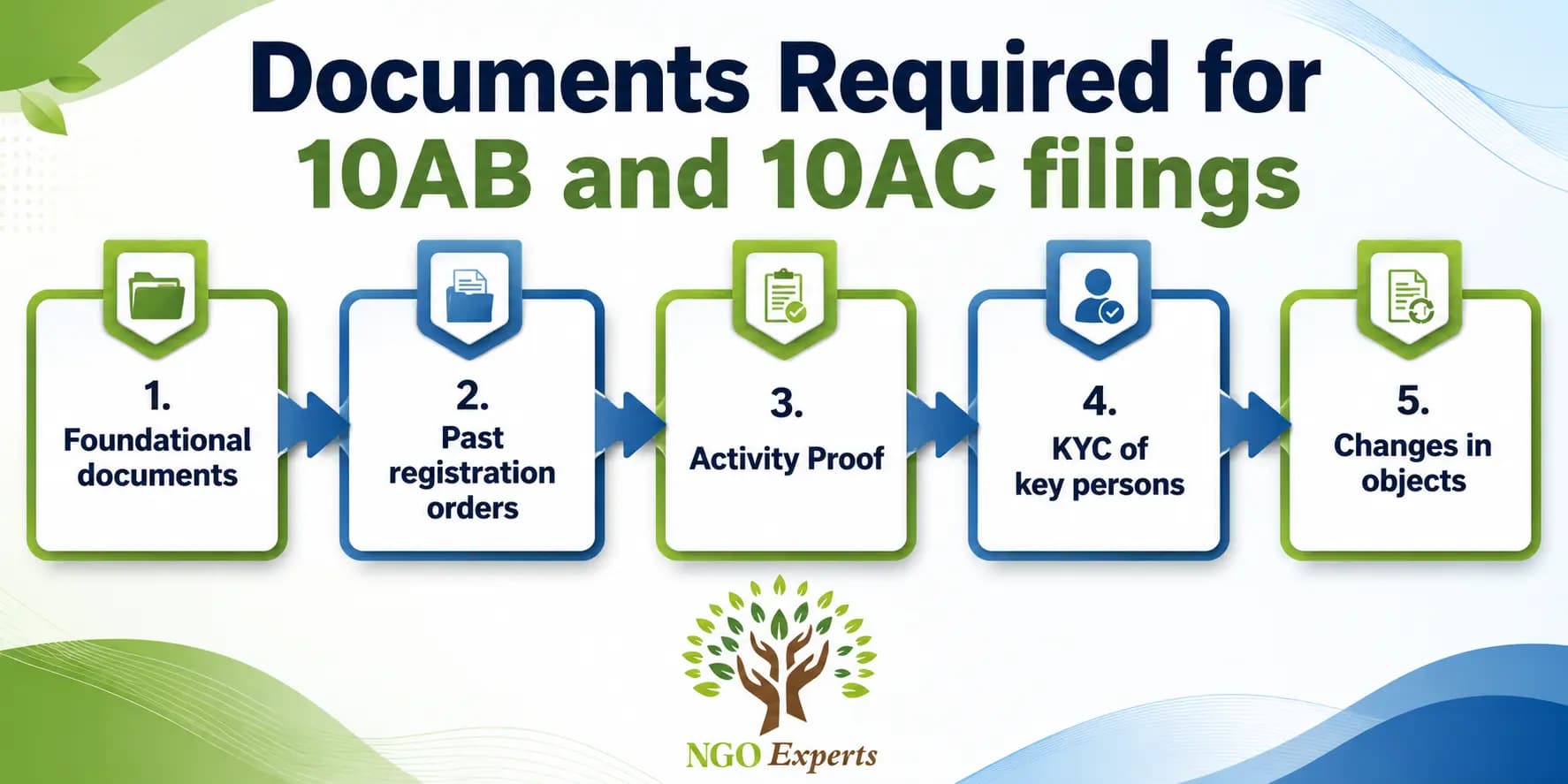

Documents Required for 10AB and 10AC filings

While the exact list can vary case by case, most NGOs and trusts will need the following documents.

Foundational documents

- Self‑certified copy of Trust Deed

- Society Memorandum & Rules

- Section 8 Company MOA/AOA.

Past registration orders

- Copy of existing registration/approval under 12A / 12AB / 10(23C) / 80G, if any.

- Financial statements

- Audited financials for up to the last 3 years, along with balance sheet, income and expenditure account, and receipts & payments.

Activity Proof

- Details of activities,

- annual reports

- photographs of the project

- evidence of charitable work and utilisation of funds

KYC of key persons

- PAN, Aadhaar, and basic details of trustees/directors/office bearers.

Changes in objects

- Documents showing modifications to objects and resolutions approving changes.

For first‑time registration leading to 10AC, similar documents are required when you apply through the initial application form.

Step‑by‑step filing process for Form 10AB

You may apply through the Income Tax portal by selecting the form, uploading supporting documents, and completing the digital verification process.

- Prepare documents and check timelines.

- Confirm whether you are converting provisional to regular, renewing, re‑registering after object change, or activating inoperative registration.

- Ensure financials, activity reports, and existing orders are ready and self‑certified.

- Select Form 10AB and the correct section.

- Choose Form 10AB from the form list and select the applicable section (10(23C), 12AB, 80G, or relevant combination).

- Choose the correct purpose: conversion, renewal, activation or re‑registration.

- Fill in organisation and activity details

- Enter basic information (name, address, legal form, registration details).

- Provide details of charitable activities, objects, geographical coverage, and utilisation of funds.

- Upload documents

- Attach trust deed/MOA, registration certificates, past approval orders, audited accounts, and KYC documents.

- Ensure files are in the prescribed formats and clearly readable.

- Verify and submit

- Review all details carefully; errors here can delay or risk approval.

- Submit using DSC or Aadhaar‑based verification, as applicable.

- Track status and respond to notices

- The Commissioner will process and, if satisfied, issue the renewal or approval order.

Filling of Form 10AC

When you file your first‑time application, the Commissioner can take the following actions.

- Scrutinises your founding documents, activities and financial projections.

- Issues an electronic order in Form 10AC either granting provisional/regular registration or rejecting with reasons.

You can verify the registration granted via 10AC on the income‑tax portal under “Verification of Trust Registration” by entering your PAN.This 10AC order must be preserved and shared with donors, CSR partners and auditors as proof of tax‑exempt registration.

Relation Between Form 10AC, 12A/12AB, and 80G

These three terms are interconnected in NGO taxation and compliance, but each serves a different purpose.

| Term | Meaning | Main Purpose | Benefit |

| 12A / 12AB Registration | Income tax exemption registration for NGOs | Exempts NGO income from tax | NGO saves tax on its income |

| 80G Registration | Donation tax deduction approval | Allows donors to claim tax deductions | Encourages donations |

| Form 10AC | Approval certificate issued by Income Tax Department | Confirms approval of 12AB and/or 80G | Acts as official proof of registration |

Final Understanding

- 12AB helps the NGO avoid paying income tax.

- 80G helps donors save tax on donations.

- Form 10AC is the legal document that confirms these approvals.

Common mistakes in 10AB and 10AC compliance

NGOs and trusts frequently overlook these points, which can delay or jeopardise the process.

Missing renewal/conversion deadlines

Not applying through 10AB at least 6 months before expiry or within 6 months of starting activities for provisional registrations.

Wrong form or wrong section selected

Selecting the incorrect section (only 12AB instead of the combined 12AB + 80G) or choosing the wrong purpose in 10AB.

Incomplete or inconsistent documents

Financials not audited, mismatch in names or PAN between deed and PAN records or objects in deed not matching claimed charitable categories.

Not reporting a change in objects.

Modifying purposes in the trust deed or MOA without applying for re‑registration via 10AB and without informing the Commissioner.

Assuming lifetime registration

Continuing to claim exemption based on the old 12A / 80G / 10(23C) orders without re‑registration under the new regime.

A professional review from NGOExperts before filing can prevent these avoidable errors.

Penalties and consequences of non‑compliance

If you do not comply properly with 10AB/10AC‑related requirements:

Cancellation or lapse of registration

Registration under Section 12AB / 10(23C) / 80G can be cancelled or allowed to lapse if you miss timelines or violate conditions.

Taxability of income

Once registration is cancelled or lapses, your income may be taxed as that of a normal entity, and benefits under Sections 11 and 12 may not be available.

Loss of donor benefits

Donors may lose their Section 80G deduction, which directly affects your fundraising and CSR prospects.

Investigations for specified violations

The Finance Act 2022 empowers authorities to examine “specified violations” and cancel registration where misuse is found.

Practical reputational risk

Non‑compliance signals weak governance to corporates, grant‑makers and foreign funders, making future funding more difficult.

Timely 10AB filing and careful 10AC‑based compliance are therefore essential to protect your NGO’s funding and credibility.

Conclusion

10AB and 10AC are two sides of the same tax‑exemption system for Indian NGOs and trusts. 10AC grants initial registration, while 10AB sustains it through conversion, renewal and re‑registration.If you use them correctly and on time, they help you enjoy continuous exemption under Sections 10(23C), 12AB and 80G, protect donor benefits and strengthen your eligibility for CSR and foreign funding. If you treat them casually, it may result in losing registration and significant fundraising challenges.

Frequently Asked Questions

Is 10AB a section or a form under the Income Tax Act?

10AB commonly refers to Form 10AB, an online form used to apply for conversion of provisional registration, renewal, activation of inoperative approval, or re‑registration under Sections 10(23C), 12AB, and 80G.

What is the difference between Form 10A, 10AB and 10AC?

Form 10A is typically used only once for first‑time registration; after that, the Commissioner issues the registration order in Form 10AC.For subsequent renewal, conversion or re‑registration, you must file Form 10AB.

When should an NGO with provisional registration file Form 10AB?

An NGO with provisional approval may file Form 10AB within 6 months of commencing activities or at least 6 months before provisional approval expires to convert to regular registration.

Can we receive CSR without 10AC/10AB-based registration?

Most CSR-funding corporates and major donors insist on valid, up‑to‑date registration under Sections 12AB and 80G, as evidenced by 10AC and renewed through 10AB, before releasing funds.

What if we changed our NGO’s objects but did not file 10AB?

If you modify objects without applying for re‑registration under 10AB and informing the Commissioner, it may be treated as a specified violation and may result in cancellation of registration.

Author

Aabha Garg

A Content Strategist at NGOExperts, who focuses on NGO registration, 12A and 80G registration, FCRA compliance, income tax filing for non-profits, and CSR funding guidelines in India. I research and write our compliance guides in collaboration with our in-house Chartered Accountants and Company Secretaries, so every article reflects current tax and regulatory requirements for the NGO and non-profit sector.

Written by Aabha Garg. Last updated on June 1, 2026