Quick Summary:

Section 135 of the Companies Act, 2013, mandates CSR implementation in India for qualifying Indian companies. An effective CSR requires careful planning, compliance, and solid partnerships that extend beyond simply making monetary donations. Regardless of company size, a solid CSR strategy aligns social initiatives with business values and drives real, lasting change. By following a structured process, companies can build programs that meet legal requirements while promoting sustainability.

NGOExperts is among India’s top CSR implementation services that help your organisation fulfil legal obligations while maximising social impact and transparency.

What is CSR Implementation?

CSR implementation is the process of planning, executing, monitoring, and reporting corporate social responsibility initiatives in Indian companies. It involves implementing meaningful programs in areas such as education, healthcare, environmental sustainability, poverty alleviation, and rural development that align with your company's values and Schedule VII activities.

Benefits of CSR Implementation in India

- It supports your company in avoiding penalties and ensures 100% adherence to the Companies Act requirements

- A professional CSR Implementation program builds brand credibility and public trust through transparent social initiatives

- It enhances overall Tax Efficiency by proper documentation and eligible spending under CSR provisions

- CSR implementation demonstrates a commitment to sustainable and ethical business practices

- It helps boost employee engagement through meaningful volunteer opportunities

- Support long-term solutions for social and environmental challenges

- Enable local organisations and beneficiaries to achieve success and scalability.

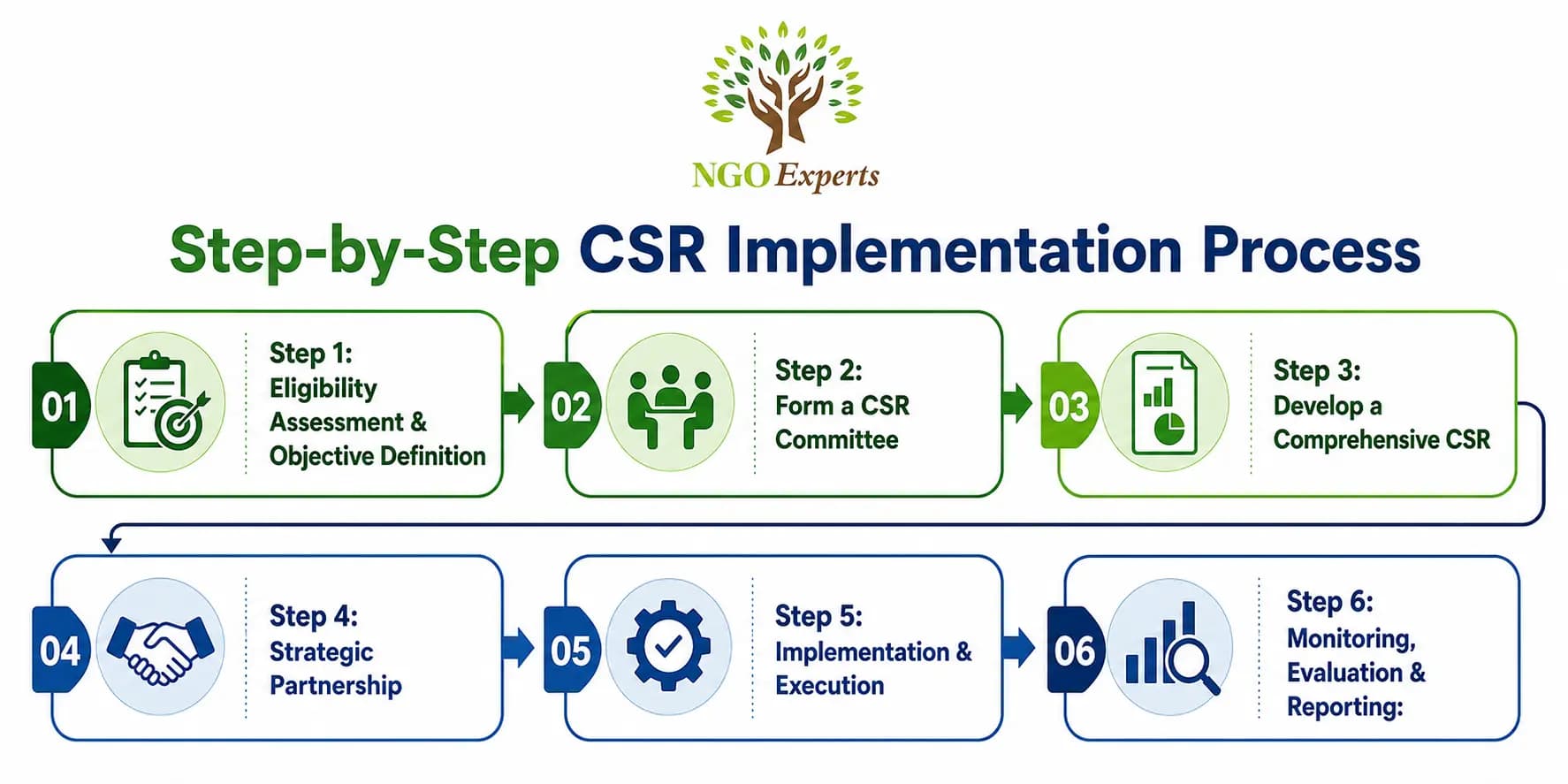

Step-by-Step CSR Implementation Process

Step 1: Eligibility Assessment & Objective Definition

Companies must implement CSR if their net worth is ₹500 crore or more, and also ensure that CSR goals must align with Schedule VII activities.

Step 2: Form a CSR Committee

Make sure it has a minimum of 3 directors who can effectively allocate budgets (minimum 2% of the average net profits of the preceding 3 years) while monitoring implementation and ensuring compliance

Step 3: Develop a Comprehensive CSR

Policy focusing on Schedule VII activities, implementation mode, and budget allocation.

Step 4: Strategic Partnership

With the right partner, focusing on core business while ensuring impact. These are the reference parameters for selecting partnerships

Verification Checklist:

- Registration with the Ministry of Corporate Affairs (MCA)

- Minimum 3 years of operational track record

- Valid 12A and 80G certifications (for tax benefits)

- Demonstrated expertise in your chosen focus area

- Financial transparency and audit reports

- Past CSR project portfolio and references

Step 5: Implementation & Execution

Direct Implementation:

- The company executes projects through its own team

- Suitable for initiatives closely related to business operations

- Requires dedicated resources and local presence

Partnership-Based Implementation:

- Leverage NGO/social enterprise expertise

- Broader reach with established community networks

- Shared risk and resources

Step 6: Monitoring, Evaluation & Reporting:

It can be done by establishing a structured KPIs showing-

- Monthly partner reports with photographic evidence

- Quarterly field visits by the CSR team

- Third-party impact assessments (annually)

- Beneficiary feedback surveys

- Social audit by independent agencies

CSR Implementation Requirements & Process

| Aspect | Requirement | Timeline |

| Eligibility Criteria | Net worth ≥₹500 cr OR Turnover ≥₹1,000 cr OR Net profit ≥₹5 cr | Preceding financial year |

| CSR Committee | Minimum 3 directors (1 independent) | Within 6 months of meeting criteria |

| CSR Policy | Board-approved, website published | Before the first CSR expenditure |

| Spending Obligation | 2% of average net profits (last 3 years) | Each financial year |

| Unspent Amount | Transfer to the specified funds or company account | Within 6 months of the FY end |

| Annual Reporting | CSR report in Board's Report (AOC-4) | With annual financial statements |

| Partner Registration | MCA-registered implementing agencies | Before project commencement |

| Impact Assessment | For projects ≥₹1 crore (if 3+ years old) | Before project |

Quick Tips for Successful CSR Implementation

Before You Start

- Conduct a baseline assessment: Understand community needs before designing projects

- Engage employees: Survey staff to identify causes they're passionate about

- Think long-term: 3-5 year programs create a deeper impact than one-off initiatives

- Budget realistically: Include monitoring, evaluation, and admin costs (up to 5% allowed)

Why Choose NGOExperts

- Expert Guidance: Our team of experienced professionals specialises in CSR implementation support, ensuring compliance with all legal requirements under the Companies Act 2013.

- Seamless Online Process: Complete your CSR committee formation online from anywhere in India. Our digital platform makes the entire process paperless and convenient.

- Comprehensive Documentation: We handle all documentation, drafting, and filing, eliminating confusion and errors that could delay your CSR formation.

- Transparent Pricing: Clear real-time project tracking and financial accountability.

- Faster Processing: Our established relationship with ROC offices and streamlined processes ensures quicker approvals and incorporation.

- 10+ Years Experience: We take pride in successfully serving 100+ companies across sectors with successful CSR programs

Frequently Asked Questions

What happens if our company doesn't spend the mandatory 2% on CSR?

Unspent CSR amounts must be transferred to specified funds within 6 months of the FY end for ongoing projects. For other cases, unspent amounts go to Schedule VII funds.

Can CSR funds be used for activities outside India?

No. CSR activities must be undertaken in India only. However, the training of Indian sports personnel representing India or internationally can be supported.

Are donations to political parties considered CSR?

No. Activities benefiting only employees and their families, political contributions, sponsorships for commercial purposes, and one-off events like awards/donations to individuals are not considered CSR.

Can we carry forward excess CSR spending to the next year?

No. Excess spending cannot be adjusted against future CSR obligations. Each year's spending must meet that year's 2% requirement independently.

What are Schedule VII activities in simple terms?

Schedule VII lists 16 permissible CSR focus areas, including education, healthcare, poverty alleviation, gender equality, environmental protection, rural development, armed forces support, sports promotion, heritage protection, disaster relief, and more.

Are CSR expenses tax-deductible?

No. CSR expenditure is NOT eligible for tax deduction under Section 80G. It's spent from post-tax profits and doesn't reduce your tax liability. This is to ensure CSR remains a genuine social contribution, not a tax-saving tool.

Author

Srijita Chatterjee

I am a Content Specialist holding a Master’s degree and with over 5 years of experience in the creative arena. I specialize in breaking down complex concepts into clear, understandable insights that help my viewers deeply engage and retain. Known for my approachable and engaging style, I am committed to providing accurate, trustworthy information that empowers individuals and organizations to make informed decisions and achieve their goals.

Written by Srijita Chatterjee. Last updated on June 5, 2026