Quick Summary

Corporate Social Responsibility (CSR) compliance in India can sound legal and complicated, but once broken down into steps, it becomes simple, structured, and manageable. For companies in India, Corporate Social Responsibility (CSR) has shifted from a voluntary act of charity to a compulsory obligation for companies that cross certain financial thresholds under Section 135 of the Companies Act, 2013.

You form a CSR Committee, prepare a CSR Policy aligned with Schedule VII activities and spend at least 2% of your average net profits from the last three years on approved projects. For unspent amounts, transfer ongoing project funds to a special account and non-ongoing to government funds, then report it all in your Board's Report and Form CSR-2 to stay penalty-free. Missing a single compliance step can lead to heavy penalties and destroy your brand reputation.

At NGOExperts, we specialise in bridging the gap between corporate goals and social impact. This guide is your ultimate CSR Compliance Checklist to ensure your company stays on the right side of the law while making a real difference.

What is CSR compliance

CSR (Corporate Social Responsibility) means that a company spends a part of its profits on activities that benefit society, such as health, education, the environment, and rural development, as listed in Schedule VII of the Act. CSR compliance is the legal requirement that companies meeting Section 135 thresholds must spend, monitor, and report CSR activities as per the Act and Companies (CSR Policy) Rules, 2014.

CSR is no longer only a moral responsibility; it is a statutory obligation with clear rules on eligibility, minimum spending, governance, reporting and penalties for non‑compliance.

Which companies must comply with CSR provisions?

CSR becomes applicable if, in the immediately preceding financial year, your company meets any one of these criteria:

- Net worth: ₹500 crore or more; or

- Turnover: ₹1,000 crore or more; or

- Net profit: ₹5 crore or more.

These limits apply to:

- Indian companies (private and public)

- Holding, subsidiary and certain foreign companies with a branch or project office in India, if they meet the Section 135(1) thresholds.

Once you initiate CSR applicability, CSR provisions normally continue until you do not meet the criteria for a continuous period, as per the Ministry of Corporate Affairs (MCA) guidance.

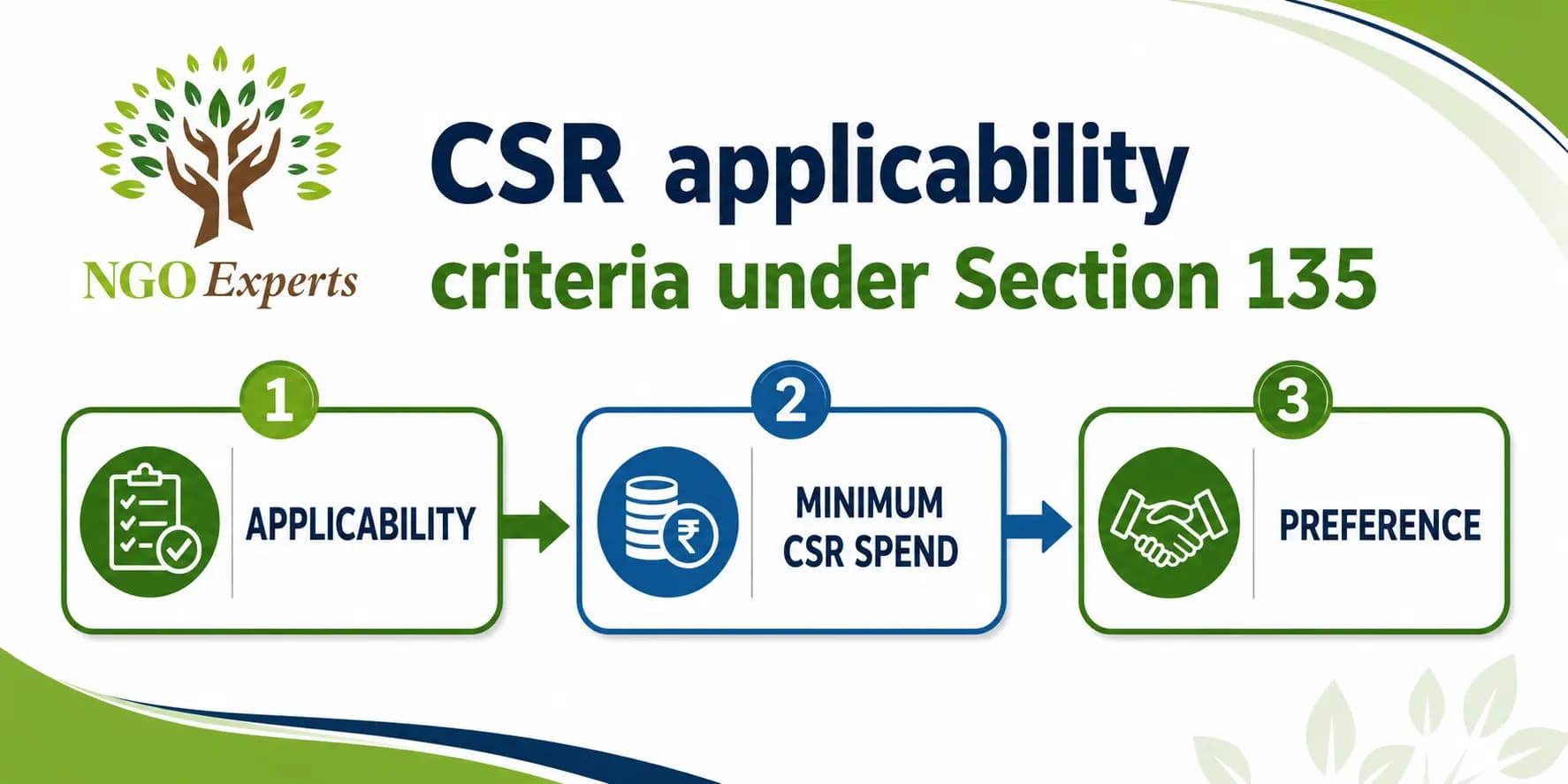

CSR applicability criteria under Section 135

Section 135 of the Companies Act, 2013, established certain rules and regulations for the CSR framework:

- Applicability: Companies meeting any of the 3 financial limits above during the immediately preceding financial year.

- Minimum CSR Spend: At least 2% of average net profits of the 3 immediately preceding financial years, calculated as per Section 198.

- Preference: The company should prioritise local areas around its operations when selecting CSR projects.

Benefits of Corporate Social Responsibility

CSR boosts brand image by aligning companies with social good, fostering customer loyalty as consumers prefer ethical brands. It also attracts top talent seeking purpose-driven employers. Key benefits are as follows.

Employee Impact

Strong CSR programs increase employee motivation and productivity by fostering shared values and providing volunteering opportunities. This creates a positive workplace, reducing recruitment costs and improving retention rates.

Business Growth

CSR aids risk management by ensuring regulatory compliance and mitigating reputational issues. It opens new opportunities via partnerships with NGOs and communities, differentiating companies in competitive markets.

Financial Upside

Companies see revenue growth from loyal customers and investors favouring sustainable firms.

| Benefit Category | Specific Gains | Example Impact |

| Reputation | Brand loyalty, trust | Consumer preference for ethical brands |

| Talent | Engagement, retention | Attracts talented employees |

| Operations | Risk reduction | Compliance avoids penalties |

| Opportunities | Partnerships, markets | NGO collaborations |

Step‑by‑step CSR compliance checklist for companies

Here are some simple steps you can follow for your company’s CSR compliance in India.

- Check CSR applicability every year.

- Compare your last financial year’s net worth, turnover and net profit with Section 135 thresholds.

- If any one limit is exceeded, CSR applies for that year.

- Constitute the CSR Committee

- For most companies: at least 3 directors, including at least 1 independent director.

- For certain companies with CSR obligations of less than Rs. 50 lakh, the Board itself may perform the functions of the CSR Committee. However, companies with unspent CSR funds for ongoing projects must maintain a CSR Committee in accordance with the 2022 amendments.

- Determine the CSR obligation (2% amount)

- Compute the average net profit of the last 3 financial years as per Section 198.

- Calculate 2% of this amount: this is your minimum CSR spend for the current year.

- Prepare the CSR Policy

- Draft CSR Policy covering focus areas, approach, implementation, monitoring and treatment of surplus; ensure it aligns with Schedule VII.

- Get recommendations from the CSR Committee and Board approval.

- Identify CSR projects and the implementation mode.

- Decide whether to implement directly or through eligible implementing agencies (registered Section 8 companies, registered public trusts, societies with a CSR registration number).

- Ensure projects clearly fall under Schedule VII activities.

- Prepare Annual Action Plan (where required)

- The CSR Committee recommends an annual action plan comprising a list of approved projects, an implementation schedule, a monitoring mechanism, and a needs & impact assessment.

- Open and manage an Unspent CSR Account.

- For ongoing projects, the unspent amount at year‑end must be transferred within 30 days to a special Unspent CSR Account and utilised within 3 financial years.

- Ensure CSR spending and documentation.

- Spend at least 2% of average net profits on eligible CSR activities within the prescribed time.

- Maintain project‑wise records, including agreements, invoices, utilisation certificates, and impact assessment reports.

- Board’s Report disclosures and CSR‑2 filing

- Disclose CSR details in the Board’s Report, including composition of CSR Committee, CSR Policy, amount required and actually spent, reasons for shortfall, and project‑wise details as per CSR Rules.

- File Form CSR‑2 with MCA within the prescribed due date (generally aligned with AOC‑4 )

CSR compliance checklist for private & public companies

This checklist is relevant for both private limited and public companies once Section 135 is applied.

| Area | Action point | Private company note | Public company note |

| Adequacy | Check Section 135 thresholds each year | The same financial criteria apply | The same financial criteria apply |

| CSR Committee | Constitute the CSR Committee as per the Act (or Board to perform functions where allowed) | May not require an independent director in some cases | Usually needs at least 1 independent director |

| CSR Policy | Draft / update CSR Policy and publish on website (if any) | Required once CSR applies | Required once CSR applies |

| CSR Budget | Calculate 2% of the average net profit of the last 3 years | Same formula | Same formula |

| Project selection | Choose Schedule VII‑compliant activities and agencies | Can be implemented directly or via eligible agencies | Same options, often larger scale |

| Unspent amount | Transfer to Unspent CSR Account / Schedule VII funds within timelines | The same rules apply | The same rules apply |

| Reporting | Include CSR details in Board’s Report, AOC‑4 and CSR‑2 | Mandatory if CSR‑applicable | Mandatory if CSR‑applicable |

CSR spending rules and minimum contribution

- Minimum CSR spend: At least 2% of the average net profits of the company made during the 3 immediately preceding financial years.

- If the company has not completed 3 financial years, the average is calculated based on available years.

- Administrative overheads are also limited to 5% of total CSR expenditure (excluding impact assessment costs), as per the CSR Rules.

- Surplus arising out of CSR activities must be redeployed towards CSR and cannot be treated as business profit; it may be ploughed back into the same project, transferred to the Unspent CSR Account, or spent as per the CSR Policy within the timelines.

If the company fails to spend the required amount, the Board must specify the reasons in its report and handle the unspent amount in accordance with Sections 135(5) and (6).

Treatment of unspent CSR amount

1. Unspent on ongoing projects

- Transfer unspent amount for ongoing projects to a special Unspent CSR Account in a scheduled bank within 30 days from the end of the financial year.

- Utilise this amount for the concerned ongoing projects within the next 3 financial years.

- Any amount remaining unspent after 3 years must be transferred to a fund specified in Schedule VII within 30 days from the end of the 3rd financial year.

2. Unspent on non‑ongoing projects

- Where the amount does not relate to an ongoing project, the company must transfer the unspent amount to a fund specified in Schedule VII within 6 months from the end of the financial year.

The board must also disclose reasons for not spending the CSR amount in its report.

CSR reporting and disclosure requirements

CSR has detailed reporting requirements for transparency and accountability.

Key disclosures include:

- In Board’s Report:

- CSR applicability and composition of the CSR Committee.

- CSR Policy and web‑link (if website exists).

- Amount required to be spent and amount actually spent during the year.

- Details of ongoing and other CSR projects, mode of implementation, and implementing agencies.

- Reasons for any unspent amount and transfer details.

- On the company website (if any): CSR Policy, CSR projects and composition of CSR Committee.

- In MCA Form CSR‑2: electronic reporting of CSR data to MCA as per the prescribed format and due dates.

Penalties for non‑compliance with CSR provisions

Non‑compliance can attract monetary penalties under the Act and CSR Rules

- Failure to transfer unspent CSR amounts to the Unspent CSR Account or Schedule VII Fund within the time limit can result in penalties against the company and its defaulting officers.

- Incorrect or delayed CSR‑2 filing may attract penalties under Sections relating to financial statements and reporting, such as Section 134(8) and relevant rules.

- Persistent non‑compliance can also damage brand reputation, stakeholder trust and eligibility in certain government or PSU tenders.

A complex internal CSR compliance system is therefore critical for risk management.

Common CSR compliance mistakes to avoid

You should avoid making the following mistakes:

- Treating staff welfare or regular HR activities as CSR, even when they benefit only employees and their families.

- Sponsorship spending is primarily aimed at marketing or brand promotion and is counted as CSR.

- Missing transfer timelines for unspent CSR amounts, especially confusion between ongoing and non‑ongoing projects.

- Weak documentation of CSR projects, agreements, utilisation certificates and impact assessment reports.

- Not aligning CSR projects strictly with Schedule VII language.

- Delayed or incorrect CSR‑2 filing and incomplete disclosures in the Board’s Report.

Professional guidance from our Experts can help you design a compliant CSR framework from day one.

Frequently Asked Questions

Is CSR mandatory for all companies in India?

CSR is mandatory only for companies that meet the financial thresholds in Section 135.

How do I calculate the 2% CSR amount?

You must calculate the average net profit of your company for the 3 immediately preceding financial years as per Section 198, and then compute 2% of that amount.

Can we do CSR through our own NGO?

Yes, CSR may be implemented through Section 8 companies, registered public trusts, or societies with a CSR registration number.

What if we cannot spend the full CSR amount in a year?

You must disclose reasons in the Board’s Report and transfer unspent amount to the Unspent CSR Account (for ongoing projects).

Are donations to any charity automatically counted as CSR?

No. Only activities that fall within Schedule VII and follow CSR Rules (including implementation route, documentation and reporting) are counted as eligible CSR.

Author

Aabha Garg

A Content Strategist at NGOExperts, who focuses on NGO registration, 12A and 80G registration, FCRA compliance, income tax filing for non-profits, and CSR funding guidelines in India. I research and write our compliance guides in collaboration with our in-house Chartered Accountants and Company Secretaries, so every article reflects current tax and regulatory requirements for the NGO and non-profit sector.

Written by Aabha Garg. Last updated on June 5, 2026