Quick Summary

If you're running a Section 8 company or just starting one, maintaining annual returns might be difficult for you, as under the Companies Act of 2013, these non-profit companies must file certain Registrar of Companies (ROC) forms, income tax reports, and other documents to remain compliant and avoid penalties. The Ministry of Corporate Affairs (MCA) and the Income Tax Department closely monitor social enterprises to ensure they use their funds for their intended purposes. To keep your NGO running smoothly, you need to follow the regulations with the following three authorities:

- ROC (MCA): For annual financial and management updates.

- Income Tax Department: To maintain your tax-exempt status.

- GST Department: Only if your commercial activities exceed a certain threshold.

At NGOExperts, our experts handle all your Section 8 annual returns, from ROC forms like AOC-4 and MGT-7 to ITR-7 filing and compliance calendars.

Annual Returns for Section 8 Company

Every year, regardless of whether you did business or not, your company must file specific documents. For Section 8 companies, the essential filings include financial statements and shareholder details. Here are some major ones:

- Form AOC-4: Your audited balance sheet, profit/loss, cash flow, and auditor's report. Due 30 days post-AGM (usually by late November if the AGM is by September 30).

- Form MGT-7: Details your structure, members, and changes over the year. File within 60 days of AGM.

- Others include ADT-1 (auditor appointment) within 15 days of the AGM and DIR-3 KYC by September 30.

- Use ITR-7 if claiming exemptions under Section 11; file audited accounts and Form 10B if needed.

ROC Forms are Required for a Section 8 Company?

Here's the list of The Registrar of Companies (ROC) filings every Section 8 company handles yearly. We've put them in a table for your ease

| Form | Purpose | Due Date (from AGM/FY End) | Key Attachments |

| AOC-4 | Financial statements | 30 days from AGM | Balance sheet, P&L, auditor report |

| MGT-7 | Annual return (structure/changes) | 60 days from AGM | Member details, board resolutions |

| ADT-1 | Auditor appointment | 15 days from AGM | - |

| DIR-3 KYC | Director KYC | Sept 30 annually | ID proofs |

| DPT-3 | Deposits return (if any) | June 30 | Deposit particulars |

| MSME-1 | MSME payments (half-yearly) | Oct 31 & April 30 | Vendor payment delays |

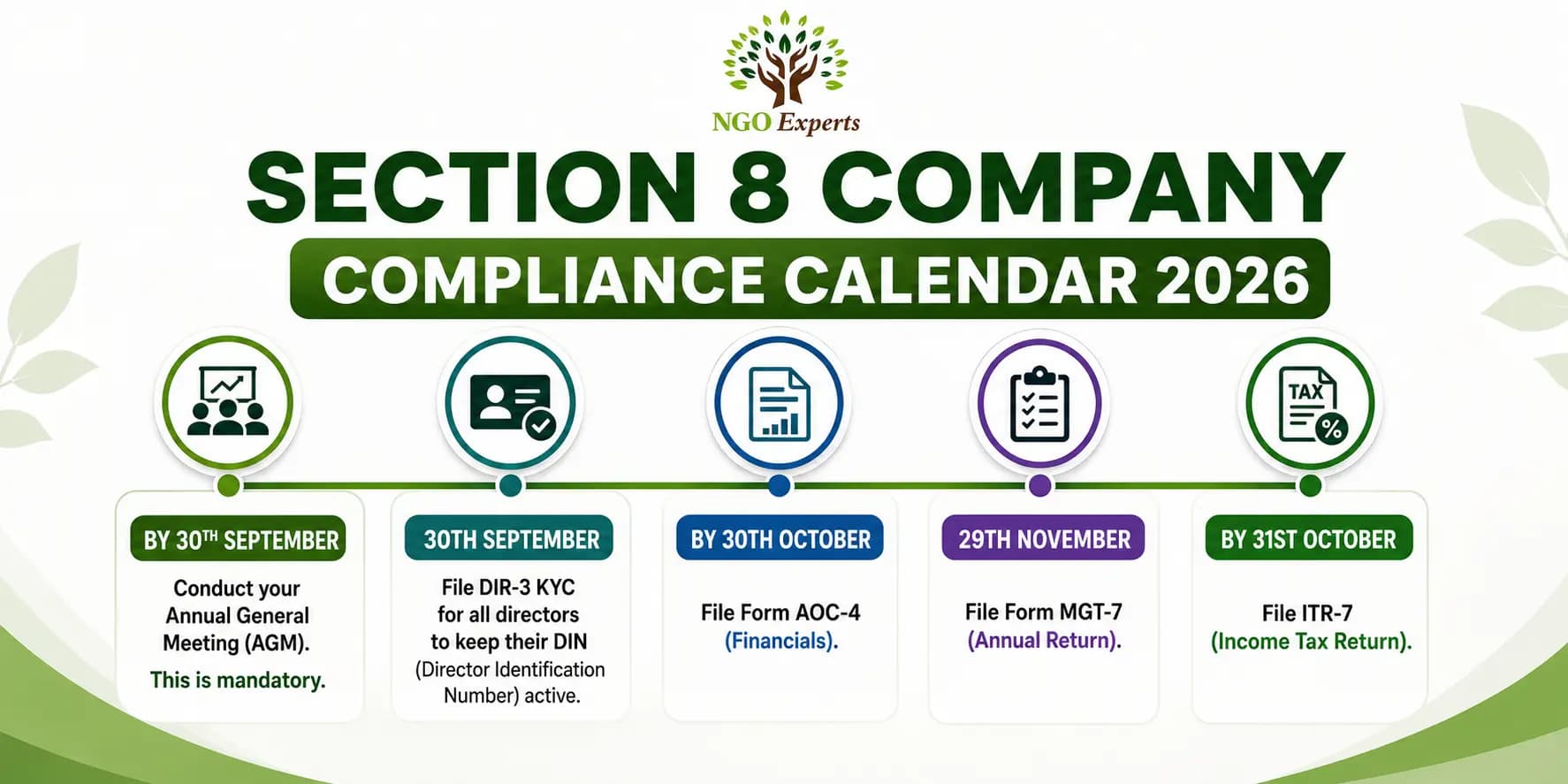

Section 8 Company Compliance Calendar 2026

Missing a date may result in heavy penalties. So mark these dates in your calendar:

- By 30th September: Conduct your Annual General Meeting (AGM). This is mandatory.

- 30th September: File DIR-3 KYC for all directors to keep their DIN (Director Identification Number) active.

- By 30th October: File Form AOC-4 (Financials).

- 29th November: File Form MGT-7 (Annual Return).

- By 31st October: File ITR-7 (Income Tax Return).

Income Tax Return (ITR) Filing Process

For Section 8 companies, filing taxes isn't always about paying tax; it’s a mandatory annual compliance to maintain your tax-exempt status.

- Audit First: Before filing, ensure your accounts are audited. If you have 12A/12AB registration, a Form 10BB audit report must be filed at least one month before the ITR deadline.

- Form Selection: Use ITR-7. This form is specifically for entities claiming exemption under Section 11 (Charitable/Religious trusts).

- Donation Reports: Don’t forget to file Form 10BD (Statement of Donations) by May 31st so your donors can get their 80G tax benefits.

GST Return Applicability

GST isn't applicable if there is no income; it applies only if taxable in the following cases:

- Registration is Mandatory: If your aggregate turnover (from selling goods or services) exceeds ₹20 lakhs (₹10 lakhs for North-Eastern states).

- Nature of Activity: If you sell products (like handicrafts or books) or provide paid services (like training workshops), GST applies just like a regular business.

- Return Frequency: If registered, you must file GSTR-1 (sales) and GSTR-3B (summary) monthly or quarterly.

Penalty for Late Filing

We are guiding you to ensure you don't miss any filing deadlines, as delays can be costly in the world of compliance.

- ROC Filing: The late fee is usually ₹100 per day per form. This can quickly add up to thousands of rupees.

- Income Tax: Filing after the due date attracts a penalty of ₹5,000 (reduced to ₹1,000 if the total income is below ₹5 Lakhs).

- Director Disqualification: A continuous default for 3 years can result in directors being disqualified and the company being shut down by the government.

Why waste your precious donations on government penalties? Partner with NGOExperts for timely, automated filing reminders and expert preparation.

Conclusion

Staying compliant might seem like a full-time job, but it is the foundation of your NGO's credibility. When your filings are up-to-date, you are more likely to receive government grants, CSR funding, and trust from individual donors.

Frequently Asked Questions

Can I skip filing if my company had zero donations this year?

No. Even if there is no activity, filing AOC-4, MGT-7, and ITR-7 is mandatory to keep the company active.

Is a Statutory Audit mandatory every year?

Yes. Every Section 8 company must have its accounts audited by a practising Chartered Accountant, regardless of turnover.

Can we pay dividends to members in a Section 8 company?

Strictly no. All profits and donations must be used only for the charitable objects of the company.

Do I need to file GST returns for donations?

Pure donations (where the donor gets nothing in return) are not subject to GST. However, if you provide advertising to the donor in exchange for payment, it may be taxable.

How many Board Meetings should we hold?

For Section 8 companies, the requirement is relaxed. You must hold at least one meeting every six calendar months.